Research results

Microfinance in Europe. Social Performance Management Report

The Report presents current state of social performance practices of European microfinance sector in implementing SPM. The main achievements of the sector are positive contribution to sustainability of microbusinesses and support to excluded segments of population. The biggest challenges industry faces are setting S.M.A.R.T. goals during SPM implementation and providing non-financial services as a development possibility.

Digitalizing Microfinance in Europe

The paper summarizes the results of the survey on the use of fintech solutions and digitalization of the customer relations and lending process among MFIs in Europe. While there is a widespread recognition about the need to use digital processes to a larger degree, the ability and willingness of MFIs to do that varies greatly. The results also show that MFIs are cautious about not losing their competitive advantage of personal relationship with their clients. Fintech and digitalization solutions should be applied based on a rational calculus of costs and benefits, in line with the mission of the organization and the needs and capabilities of the clients.

Are Microfinance Borrowers in Lebanon Over-Indebted?

The paper presents the results of the research study that aimed to provide empirical evidence that would confirm or refute indications of cross- and over-indebtedness in Lebanon, to analyze the causes of potential cross- or over-indebtedness, and to formulate recommendations on how to address these. The study was commissioned by the SANAD Fund for MSME’s Technical Assistance Facility and the Consultative Group to Assist the Poor (CGAP) and implemented by the Microfinance Centre (MFC) in collaboration with Sanabel.

The paper presents the results of the research study that aimed to provide empirical evidence that would confirm or refute indications of cross- and over-indebtedness in Lebanon, to analyze the causes of potential cross- or over-indebtedness, and to formulate recommendations on how to address these. The study was commissioned by the SANAD Fund for MSME’s Technical Assistance Facility and the Consultative Group to Assist the Poor (CGAP) and implemented by the Microfinance Centre (MFC) in collaboration with Sanabel.

Download Lebanon Over-Indebtedness Study

Microfinance and Business Start-ups: Review of the Current Practice in Europe

The paper explores the theoretical background and the emergent evidence related to the role of access to finance for business start-ups and self-employment in Europe, with a specific focus on the role of microfinance institutions. The paper summarizes opportunities and challenges faced by the microfinance sector to more deeply engage in the entrepreneurship and start-up financing market. Options for larger engagement of the microfinance institutions in the start-up segment close the paper offering several policy recommendations on the EU and individual member state levels to support a greater role of microfinance institutions in financing business start-ups by the excluded groups.

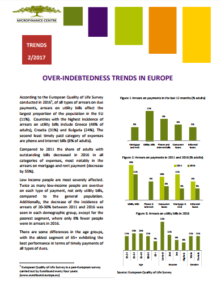

Over-indebtedness Trends in Europe – Issue No. 2

The European Quality of Life Survey (2016) shows the improving trend in the incidence of arrears on various types of dues among European households. Still, the utility bills are the largest burden, with 11% of adults in the EU-28 making late payments. Low-income people are most severely affected. Twice as many low-income people are overdue on each type of payment, not only utility bills, compared to the general population. It seems that over-indebtedness is on the decline as the incidence of arrears in general population has decreased. Despite that, microfinance institutions observe increasing over-indebtedness of their clients. In the opinion of 63% of MFIs the level of debt load of their clients increased, mostly among low-income households.

The European Quality of Life Survey (2016) shows the improving trend in the incidence of arrears on various types of dues among European households. Still, the utility bills are the largest burden, with 11% of adults in the EU-28 making late payments. Low-income people are most severely affected. Twice as many low-income people are overdue on each type of payment, not only utility bills, compared to the general population. It seems that over-indebtedness is on the decline as the incidence of arrears in general population has decreased. Despite that, microfinance institutions observe increasing over-indebtedness of their clients. In the opinion of 63% of MFIs the level of debt load of their clients increased, mostly among low-income households.

Delivering Financial Capability: A Look at Business Approaches

Financial capability has been a buzz word for almost a decade as more and more financial institutions and other stakeholders recognize that in order to improve financial inclusion, customers need to have the financial capability to use financial services for their benefit.

Many institutions are engaged in designing financial capability programs, however, many pilot programs, often donor-driven, have failed to scale up or integrate with the core business of the institution. CFI Fellow Justyna Pytkowska will explore the viable cases of financial capability interventions that can serve as models for other financial institutions to replicate, contributing to the identification of best practices and innovative delivery models.

Over-indebtedness trends in Europe

According to Eurostat data, the level of over-indebtedness (measured by the incidence of arrears on mortgage, rent, utility bills or hire purchase) decreased in 2016 in most EU countries. Please read our latest release with more information about this trend.

MFC Policy Paper No.5: Demystifying the role of microfinance in job creation

The paper discusses the role of microfinance in job creation through self-employment and microenterprise. Despite high expectations, in general microenterprises have a limited however socially important contribution to job creation. It is necessary to distinguish between growth-oriented young firms that have a potential to create jobs and self-employment and microenterprises which remain small. If microfinance focuses on the latter group, its impact on job creation will remain small. It may be more economical to reposition microfinance to become a more flexible micro-venture instrument that will fund job creators while leaving support for self-employment and microenterprises to other social programs, including seed capital grant funds.

MFC Research paper: Measuring Financial Inclusion in the EU: Financial Inclusion Score Approach

The paper presents a radical new approach to measuring financial inclusion in the EU: a financial inclusion score that treats financial inclusion as the efficiency with which a financial system transforms the conditions of access (infrastructure, regulations, etc) into the actual use of financial services. Why is this so important? Because it allows us to see which countries are the most efficient – and in case of efficiency laggards, the extent to which financial service use can realistically be increased, given existing conditions.

The paper presents a radical new approach to measuring financial inclusion in the EU: a financial inclusion score that treats financial inclusion as the efficiency with which a financial system transforms the conditions of access (infrastructure, regulations, etc) into the actual use of financial services. Why is this so important? Because it allows us to see which countries are the most efficient – and in case of efficiency laggards, the extent to which financial service use can realistically be increased, given existing conditions.

MFC Research paper: Financing Gap and SME Employment Growth: Beyond Access to Finance

The key aim of our research was to investigate the relation between the perceived changes in financing gap and employment growth by SMEs in the EU. The paper builds on and extends the analysis of SAFE survey data, in order to focus on the question of employment creation which is at the core of the current economic policy debate in the EU. The main finding emerging is that changes in the financing gap do not appear to constrain employment growth, but are strongly correlated with job destruction. This innovative research analyzed the role of the perception of external finance accessibility, whereas many other papers study the influence of the actual availability or actual constraints; as such this study points to an important relationship between the opinion of business owners and actual business growth.

Microfinance in Europe: A Survey of EMN-MFC Members. Report 2014-2015

This seventh edition of the Report on microfinance in Europe provides an overview of the development of the sector in terms of the main institutional characteristics, the microloan portfolio, and the social and financial performance for the period 2014-2015. The Report is based on data collected through a survey which was carried out as a collaboration between the European Microfinance Network (EMN) and the Microfinance Centre (MFC) for the first time. 149 Microfinance Institutions across 22 European countries contributed to this Report. The institutions surveyed are exclusively members of EMN and MFC or members of National Networks affiliated with EMN. The Report 2014-2015 was carried out by Fondazione Giordano Dell’Amore.

This seventh edition of the Report on microfinance in Europe provides an overview of the development of the sector in terms of the main institutional characteristics, the microloan portfolio, and the social and financial performance for the period 2014-2015. The Report is based on data collected through a survey which was carried out as a collaboration between the European Microfinance Network (EMN) and the Microfinance Centre (MFC) for the first time. 149 Microfinance Institutions across 22 European countries contributed to this Report. The institutions surveyed are exclusively members of EMN and MFC or members of National Networks affiliated with EMN. The Report 2014-2015 was carried out by Fondazione Giordano Dell’Amore.

MFC Policy Paper No.4: Too Little or Too Much Credit: Small Business Indebtedness in the EU, 2015

The paper reviews the potential reasons for small business indebtedness and proposes action steps to develop better understanding of the size and scale of this phenomenon in the EU. Access to finance for small businesses draws a lot of policy attention based on the premise that small businesses face credit constraints more than larger firms. While this may be true for some types of small businesses, it is also true that small businesses over-borrow and over-invest which may lead to business closures and bankruptcies. So far this aspect of small business borrowing has attracted little attention.

The paper reviews the potential reasons for small business indebtedness and proposes action steps to develop better understanding of the size and scale of this phenomenon in the EU. Access to finance for small businesses draws a lot of policy attention based on the premise that small businesses face credit constraints more than larger firms. While this may be true for some types of small businesses, it is also true that small businesses over-borrow and over-invest which may lead to business closures and bankruptcies. So far this aspect of small business borrowing has attracted little attention.

MFC Policy Paper No. 3: Of Mice and Unemployed: Rethinking Micro-Enterprise and Small Business, 2015

Policies in the EU The paper discusses the complex relationships between firms size and job creation in the EU which shows that there is a need to better understand the dynamics of the job creation and destruction process. Promoting jobs through self-employment and small businesses is an alternative strategy that carries high hopes and attracts a lot of policy attention on the theory that small businesses create the majority of jobs in the economy. However, despite the widespread support for small business startups – from entry to the growth dynamics in the first years of their existence – their role for job creation is not well understood and the policies may be following the wrong prescriptions.

Policies in the EU The paper discusses the complex relationships between firms size and job creation in the EU which shows that there is a need to better understand the dynamics of the job creation and destruction process. Promoting jobs through self-employment and small businesses is an alternative strategy that carries high hopes and attracts a lot of policy attention on the theory that small businesses create the majority of jobs in the economy. However, despite the widespread support for small business startups – from entry to the growth dynamics in the first years of their existence – their role for job creation is not well understood and the policies may be following the wrong prescriptions.

MFC Policy paper: Debt, Borrowing and Over-indebtedness: a Country-Level Monitoring Framework, 2014

MFC Policy paper: Debt, Borrowing and Over-indebtedness: a Country-Level Monitoring Framework, 2014

A review of debt burden and over-indebtedness issues shows that debt is a very complex phenomenon, which has economic impact on growth, and a social impact on the well-being of individuals and households. A lot of research and data is available on the topic offering insights into different aspects of indebtedness. What is missing is a higher level, “big picture” approach to consolidate these various strands of findings and policy initiatives, and provide higher level guidance for policy-makers and advocacy groups. The paper proposes setting up “Debt Watch” mechanism in each country for systematic revision of national policies, actions and gaps in addressing over-indebtedness issues.

Measuring Financial Inclusion in the EU: the New “Financial Inclusion Score”, 2014

Measuring Financial Inclusion in the EU: the New “Financial Inclusion Score”, 2014

This paper proposes a synthetic measure of financial inclusion. A new “Financial Inclusion Score” (or FIS) uses endogenous weights for inputs and outputs, using a data envelopment analysis (DEA) method. Using these FIS scores, this paper discusses the financial inclusion ranking of 27 EU countries, and suggests how this measure can be used by national and EU policymakers for advancing financial inclusion.

Financial Inclusion of Individuals in Poland

Financial Inclusion of Individuals in Poland

Full text in Polish, executive summary in English

Results of the desk review presentation in Polish, in English

The executive summary presents the main results of the research on financial inclusion of individuals in Poland thus providing insight into the level of usage of various financial products and services as well as into the conditions of access. The Index of Financial Inclusion (IFI) calculated for Poland captures in a summary form the progress in setting appropriate conditions to improve financial inclusion.

Measuring Financial Inclusion in Turkey

This briefing paper summarizes the current state of financial inclusion in Turkey in terms of financial services usage and the level of access to financial services for individuals and SMEs.

Measuring Access to Finance: Developing Evidence-Based Access Policies

Measuring Access to Finance: Developing Evidence-Based Access Policies

Access to Finance Scorecard (AFS) framework captures diverse aspects of access and usage issues into one comprehensive tool that lends itself to measurement and interpretation that can inform policy making and regulation of financial services. The ‘balanced’ aspect of AFS lies in the fact that it takes into account not only the facts about the supply of and demand for financial services in the traditional way, but also incorporates many other important factors that influence the participation in financial markets by households and firms such as trust in financial institutions, business confidence, financial capabilities and other subjective factors, in addition to the critical assessment of financial sector environment and policies (from the point of view of access) that influence the use of financial services.

The Level of Indebtedness of MSME Credit Customers and the Quality of Finance in Bosnia and Herzegovina

The Level of Indebtedness of MSME Credit Customers and the Quality of Finance in Bosnia and HerzegovinaThis report analyses the level of indebtedness of MSME credit customers and the quality of finance in Bosnia and Herzegovina (BiH). The EFSE Development Facility (DF) commissioned this study in February 2013, following a first study by the EFSE DF on the subject in 2009. The first study (Maurer/Pytkowska, 2010) confirmed the presence of over-indebtedness as defined by the authors, among microcredit borrowers in BiH. The findings show that the majority of borrowers have more than one credit product outstanding. Moreover, multiple and cross-borrowing are still prevalent albeit to a lower degree compared to the 2009 microcredit data sample and high levels of indebtedness still prevail in certain market segments.

Rynek pracy i wykluczenie społeczne w kontekście percepcji Polaków. Diagnoza Społeczna 2015

Rynek pracy i wykluczenie społeczne w kontekście percepcji Polaków. Diagnoza Społeczna 2015

Piąty tematyczny raport ukazujący zagadnienia związane z rynkiem pracy i wykluczeniem społecznym w kontekście percepcji Polaków

Diagnoza społeczna 2015. Warunki i jakość życia polaków. Rozdizał 4.3. Zasobność materialna

Diagnoza społeczna 2015. Warunki i jakość życia polaków. Rozdizał 4.3. Zasobność materialna

- Tackling the Effects of Crisis in Microfirms in Poland, 2013

- Social Innovations in Microfinance, 2012

- Microentrepreneurs – to Conquer or Survive? Presentation in Polish

- The Risk of Over-indebtedness of Microcredit Clients in Azerbaijan,2012

- Estimation and Analysis of Financial Inclusion among Households and Individuals in the Republic of Belarus. Full text, summary

- Estimation and Analysis of SME Financial Inclusion in the Republic of Belarus. Full text, summary

- Financial Inclusion Policy Survey in the Republic of Belarus.

- Assessment and analysis of Supply of Financial Services to individual consumers in Belarus. Full text, summary

- The impact of matched savings scheme on financial behavior of financial education training participants,2011

- The impact of reminders on financial behavior of financial education training participants, 2011

- Research on Value Chains in Kyrgyzstan and Tajikistan, 2011

- Research on the Level of Indebtedness and Repayment Performance of Individual Borrowers in Kyrgyzstan, 2011 (in English, in Russian) Presentation (in English, in Russian)

- Indebtedness of Microcredit Clients in Kosovo, 2011 Sumarry paper (in English, in Russian, in Albanian)

- Financial Condition of Microenterprises after the Crisis (Poland), 2011

- The Market for Deposit Services of Microcredit-Deposit Organizations (MDO) in Tajikistan, 2010

- Indebtedness of Microcredit Clients in Bosnia and Herzegovina, 2010 (in English, in Russian)

- Re-emerging from the Crisis – Microfinance in ECA, 2010

- Microfinance in ECA on the Eve of Financial Crisis, 2009

- Market for Microinsurance in Armenia. Low-Income Households Needs and Market Development Projections, 2009

-